")

The world’s biggest firms

Sep 21st 2013

American private enterprise dominates the corporate premier league again, thanks to waning valuations of state-backed firms

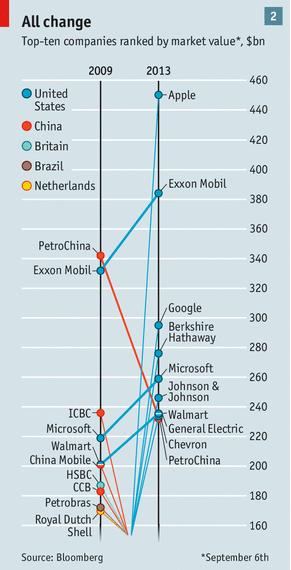

BACK in September 2009 it seemed that America Inc was being crushed. Of the world’s ten largest quoted firms by market value, only three were American—Exxon Mobil, Microsoft and Walmart. The list was dominated by state-controlled giants such as PetroChina, China Mobile and ICBC, a Chinese bank. Petrobras, an oil-and-gas firm run by the Brazilian government, had just made it into the ninth slot. It all fitted an easy story. America was in decline after the subprime crisis. The private firm was being displaced by state capitalism. There was an inexorable shift in power to the emerging world.

Related topics

• Petroleo Brasileiro

• Exxon Mobil

• Verizon

• Microsoft

• PetroChina

That year turned out to be a low point for the American firm: its resurgence has been remarkable. Today nine of the ten most valuable companies are American. The country has not been as dominant for a decade. Look at the top 50 firms and America’s share is much lower. But it is still over 50%, and has recently begun to rise (see chart 1). With its economy energised, not least by cheap shale gas, and its stockmarket rampant there is optimism in the air. The big beasts are stirring.

On September 2nd Verizon, a telecoms firm based in New York, said it would take full control of its wireless arm, buying out its British partner, the once all-conquering Vodafone. At $130 billion this deal is the third-largest ever and an advertisement for the depth and sophistication of Western capital markets—Verizon has managed to issue a colossal $49-billion-worth of bonds and the next stage is a fiddly cross-border transfer of Verizon shares to Vodafone shareholders. The following day Microsoft said it was buying Nokia’s troubled handset arm. In its pomp thirteen years ago Nokia was the world’s 16th-biggest firm. Now America dominates the wireless industry.

Churning and earning

Countries do not need giant companies to be successful: Germany’s strength is its medium-sized firms; Canada is comfortable living colossus-free. And dominance in the league tables can evaporate quickly. In May 1987, before Japan’s banks keeled over, the country accounted for eight of the top ten companies. Tokyo Electric Power, once the planet’s third-biggest firm, is now worth a tenth of its peak value back then, and mainly famous for the disaster at its Fukushima nuclear plant.

In 2000, even as the dot-com bubble began to burst, Cisco and Oracle (two technology giants) were in the top ten. Between 2005 and 2007 Citigroup, AIG and Bank of America moved in and out of the top ten—all three had to be bailed out by taxpayers before the decade was done. As the next decade began, talk of a commodities “supercycle” driven by Chinese demand saw BHP Billiton, an Australian mining firm, join the top ten. Now it has slumped back to 27th place.

Despite a certain fickleness, though, the ranking is a snapshot of something that matters. Plenty of businesspeople believe that being among the biggest firms in a given industry matters if a company is to compete in the globalised economy. And although corporate America’s achievement is due, in part, to fashion among investors—the stockmarket and dollar have risen strongly this year—three deeper forces are also at work.

The first is America’s mix of resilience and dynamism. True, there is an old guard. Exxon, an energy producer, General Electric (GE), an industrial conglomerate, and Johnson & Johnson, a health-care outfit, were all in, or very close to, the top ten a decade ago—and between them boast four centuries of history. But the old financial establishment has bombed; America’s most valuable lender is Wells Fargo, once dismissed as a bumpkin’s bank by Wall Street types. Coca-Cola and Pfizer have slipped from the first tier, but by improving its once-dreadful exploration record Chevron has become the world’s second-most-valuable oil firm. Intel and IBM, tech stalwarts that both graced the top ten in the past decade, have ceded their spots to Google and Apple (see chart 2)—though IBM may well come back. Microsoft is the lone tech survivor. There seems to be more churn among America’s biggest companies than in the rest of the world.

The second deeper force at work is Europe’s poor performance. Switzerland and Britain still have a disproportionate share of firms in the top 50, including Nestlé, Roche, HSBC and BP. But the rest of the continent boasts only four top-50 firms. A long preference for bank financing over stockmarkets is part of the story, and the difficulty of consolidation through cross-border takeovers probably has not helped. Nor has the euro crisis. It clobbered Santander, a bank, and Telefónica, a telecoms company—Spanish firms with large Latin American operations that, five years ago, were rushing up the rankings.

The third force at work is the rise and fall of state-controlled firms, particularly Chinese ones. China Mobile listed in 1997 and in the next decade many other huge Chinese firms went public, including the country’s big banks. The frenzy peaked in 2007 when PetroChina, an oil firm that was already listed in Hong Kong and America, sold shares on the Shanghai market. It briefly became the only firm in history to have been worth over $1 trillion. If you take the highest-ever value for each of 2009’s top-ten state firms and add them together you get $3.7 trillion.

That global total has now fallen to $1.5 trillion. PetroChina is today worth just $233 billion. This epic loss clearly reflects frothy initial valuations, the decline in commodity prices and the recent sell-off in emerging markets. But it may also show that investors are growing wary of state-backed firms for more fundamental reasons.

Gazprom, a Russian energy firm run by the Kremlin, has fallen to a value just three times its annual profits, compared with 11 times for Exxon. One of China’s big three lenders, Bank of China, now trades below its book value, and the other two are not far off. China Mobile has been de-rated compared with its Asian peers, according to James Ratzer, of New Street Research, an analysis firm. Vale, a big Brazilian miner over which state-backed institutions hold sway, is cheaper than global rivals such as BHP Billiton and Rio Tinto.

This may be because the downsides to cosy relationships with government have become clearer. On September 2nd Jiang Jiemin, PetroChina’s former chairman, was put under investigation for “suspected serious disciplinary violations”, an official term that often denotes accusations of graft. Fund managers worry that China Mobile may be forced to invest in unprofitable networks for the greater national good, according to Mr Ratzer. Many investors fear that the government-induced lending boom of the past five years has left China’s banks packed with bad debts. They still salivate over Chinese public offerings—just not those of sluggish state-backed monoliths. If, as expected, Alibaba, a big privately controlled internet company, soon floats it will do so on a sky-high multiple of its profits.

It is a similar story elsewhere. The $40 billion a year which the Peterson Institute for International Economics, a think-tank, believes that Gazprom loses to graft and inefficiency may account for its collapsing share price. Minority shareholders in Brazil argue that state meddling has hurt profits by requiring Petrobras to use local suppliers, regulating retail prices and dictating the role it plays in exploiting the country’s giant offshore oilfields.

American boosters may take cheer from their home teams’ ascendancy. They should remember that at this level victory comes from away goals. Successful American companies have become more global. Six of those in the top ten—including Google—sell more abroad than at home, and in almost all cases the proportion of foreign sales is rising steadily. Jeff Immelt, GE’s boss, is prone to speculating that his successor may not be American. Among Chevron’s biggest bets is an Australian gasfield called Gorgon—not shale gas at home.

Nor is America’s new-found dominance assured. Measured using a larger sample of the top 50 firms its share is lower and the recovery less pronounced. Two state firms, ICBC and China Mobile, sit just outside the top ten. Of the firms ranked 11th to 30th fewer than half are American. Perhaps most significantly, American firms no longer dominate by profits (see chart 3). Even if their share prices have been lacklustre or worse, most giant emerging-market firms have steadily increased their earnings—China Mobile’s annual net income has almost doubled in five years to a massive $20 billion.

Written in water

Today’s investors value America’s big firms more, with respect to their incomes, than they do firms elsewhere, perhaps reflecting a belief in their ability and willingness to allocate resources efficiently and to govern themselves in a shareholder-friendly way. By improving the way they are run, other firms with large profits could boost their valuations and creep up the league table. This is true of some private-sector firms, like Volkswagen and Samsung, that have a reputation for opacity and mediocre ratings as a result. And it applies in spades to big state firms.

There are some hints of change. Petrobras has allowed minority investors to appoint a director to its board. Maria das Graças Foster, its newish boss, has indicated it will be more careful with its investments. Russia’s government has talked about making state firms pay higher dividends, in part to force greater discipline upon them. China’s reformers signal that they would like to confront its mighty industrial lobby. A 2012 semi-official report called “China 2030”, written in conjunction with the World Bank, says that allowing state firms to act in a more commercial manner is a key objective. The hybrid model which makes firms answerable to both investors and politicians may never be satisfactory, but it can be improved.

Many non-American firms have the profits needed to rise up the league table of the world’s most valuable companies. If they harness this raw financial muscle to a broader global outlook and better management and governance they will kindle, or rekindle, investors’ confidence. And America will have a fight on its hands

| < Anterior | Próximo > |

|---|